Starting a new business is exciting, but it also comes with legal and financial risks that many first-time entrepreneurs overlook. One of the most important concepts to understand early on is personal liability. It determines whether your personal assets—such as your home, savings, or vehicle—are protected if your business runs into legal or financial trouble.

Many new business owners assume that registering a business name alone is enough to separate personal and business risk. In reality, liability depends on your business structure, contracts, insurance coverage, and how carefully you manage operations. Understanding how personal liability works can help you avoid costly mistakes and build a more secure foundation for your business.

Understanding Personal Liability in Business

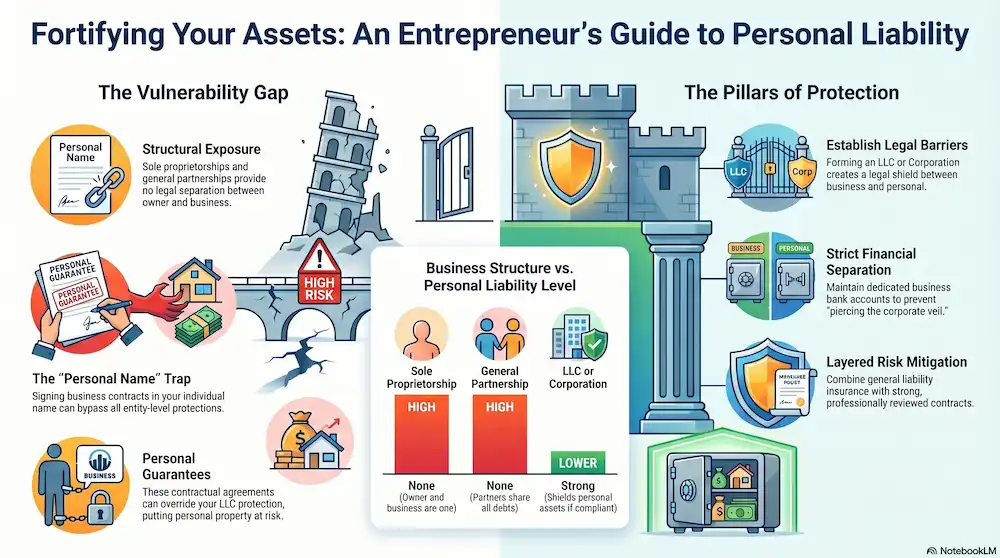

Personal liability refers to your legal responsibility for debts, obligations, or damages caused by your business. If you are personally liable, creditors or legal claims can go beyond your business assets and target your personal property.

This typically happens in sole proprietorships and general partnerships, where there is no legal separation between the owner and the business. In contrast, certain business structures can create a legal barrier that helps protect personal assets.

For example, forming a Limited Liability Company (LLC) or corporation can limit personal exposure, but only if the business is properly maintained and legally compliant.

To better understand how structure impacts protection, you can explore our Business Formation Guide for Entrepreneurs.

Why New Business Owners Are Most at Risk

New business owners are often more vulnerable to personal liability because they are still building systems, contracts, and risk management strategies. In the early stages, decisions are often made quickly, sometimes without legal review or proper documentation.

Common risk factors include signing contracts personally instead of through the business entity, underestimating operational risks, and failing to separate personal and business finances. These mistakes can make it easier for creditors or legal claims to reach personal assets.

Another challenge is lack of awareness. Many entrepreneurs assume that small businesses are naturally protected, but protection only exists when proper legal structures and safeguards are in place.

Business Structures That Affect Personal Liability

Your business structure plays a major role in determining how much personal risk you carry. Each structure offers different levels of protection and responsibility.

A sole proprietorship provides no separation between the owner and the business, meaning personal assets are fully exposed. A general partnership operates similarly, where each partner may be personally responsible for business obligations.

On the other hand, structures like LLCs and corporations are designed to create a legal separation between the business and the owner. This separation helps protect personal assets in most situations, although exceptions can apply such as fraud, negligence, or failure to follow legal requirements.

Choosing the right structure is one of the most important decisions a new business owner can make. For more guidance, visit our Guide to Choosing the Right Business Structure.

Common Situations Where Personal Liability Becomes a Problem

Personal liability issues often arise unexpectedly, especially when business operations are not properly structured or insured. Even small mistakes can lead to serious consequences.

Some common situations include signing contracts in your personal name instead of your business name, workplace accidents, unpaid business debts with personal guarantees, customer lawsuits, or compliance violations.

In these cases, legal claims may extend to personal assets if protections are weak or improperly maintained.

The Role of Business Insurance in Reducing Risk

Business insurance is one of the most effective tools for reducing personal liability exposure. While legal structures provide a foundation of protection, insurance helps cover financial losses that might otherwise become your responsibility.

General liability insurance, professional liability insurance, and commercial property insurance are commonly used to protect businesses from claims involving injury, negligence, or property damage.

However, insurance does not eliminate all risk. Policies have limits and exclusions, so they work best when combined with proper business structure and compliance practices.

Why Separating Personal and Business Finances Matters

Keeping personal and business finances separate is one of the simplest but most important ways to reduce liability risk. Mixing funds can weaken legal protections and create complications during audits or legal disputes.

Opening a dedicated business bank account, using separate credit cards, and maintaining accurate records helps establish a clear boundary between personal and business activities.

This separation also improves financial clarity, making it easier to manage taxes, expenses, and profitability.

Personal Guarantees and Hidden Liability Risks

Even with an LLC or corporation, personal liability can still arise through personal guarantees. A personal guarantee means you agree to be personally responsible for a business debt if the company cannot pay.

This is common when applying for loans, leases, or vendor agreements. Many new business owners sign these documents without fully understanding the long-term risk.

Once signed, a personal guarantee can override the protection provided by your business structure, putting personal assets at risk.

How Contracts Help Protect You From Liability

Strong contracts are essential for reducing personal liability. They clearly define responsibilities, limit exposure, and outline expectations between parties.

Without proper contracts, disputes are more likely to escalate into legal claims that can affect both business and personal assets.

Effective contracts should include payment terms, liability limitations, scope of work, and dispute resolution clauses. Having agreements reviewed by a legal professional is often a smart investment for new business owners.

Protecting Yourself From Personal Liability as Your Business Grows

Personal liability is not something new business owners can afford to ignore. As your business expands, so does your exposure to legal and financial risk. What starts as a small contract, a simple service agreement, or a minor operational decision can eventually turn into a situation where personal assets are at stake if protections are not in place.

The key to reducing risk is being proactive instead of reactive. Choosing the right business structure, maintaining clear financial separation, securing proper insurance coverage, and using well-drafted contracts all work together to create layers of protection around your personal assets. No single step is enough on its own, but combined they significantly lower your vulnerability.

As your business evolves, it is also important to regularly review your legal setup and update your protections. Growth often introduces new risks such as hiring employees, entering larger contracts, or working with higher-value clients. Each of these changes can affect your liability exposure.

By staying consistent with legal and financial best practices, you can build a business that not only grows successfully but also protects what you have personally worked hard to build.