When a small business owner passes away, their company becomes part of the probate process—a legal procedure that can delay decisions, restrict access to funds, and create uncertainty. For many small businesses, even a short disruption can lead to lost revenue, strained relationships, or long-term damage. That’s why protecting your business assets during probate isn’t just a legal concern—it’s a critical part of business continuity planning.

Learn how to safeguard your company, maintain operations, and reduce risks during probate with practical and proactive strategies.

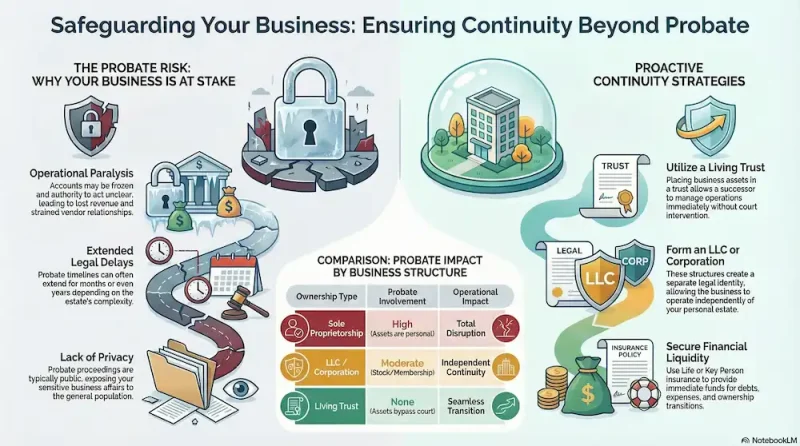

Why Probate Can Put Your Business at Risk

Probate is designed to validate a will and oversee the distribution of assets, but it often moves slowly. During this time, business accounts may be temporarily inaccessible, ownership decisions can be delayed, and authority to act on behalf of the business may be unclear.

Without preparation, your business could face operational paralysis. Employees may not know who is in charge, vendors may hesitate to continue services, and clients may lose confidence. According to resources like https://www.americanbar.org/groups/real_property_trust_estate/resources/estate_planning/probate/, probate timelines can extend for months or even years depending on complexity.

Establish a Legal Structure That Protects Your Business

If your business is still operating as a sole proprietorship, it is highly vulnerable during probate because there is no legal distinction between personal and business assets. This means your entire business becomes part of the probate estate.

Forming a limited liability company (LLC) or corporation creates a separate legal identity. This separation allows the business to continue operating independently of your personal estate, making ownership transfers smoother and reducing the risk of disruption. It also provides a clearer framework for succession and decision-making.

Create a Business Succession Plan

A well-thought-out succession plan is one of the most important tools for protecting your business. It outlines who will take over, how ownership will be transferred, and how daily operations should continue.

Instead of leaving decisions to the courts or family members who may not be prepared, a succession plan gives clear direction. It can identify a successor, define leadership roles, and provide guidance for maintaining relationships with clients and employees.

This plan should be reviewed regularly to reflect changes in your business, leadership team, or long-term goals.

Use a Living Trust to Avoid Probate Delays

One of the most effective ways to protect your business is to place it in a revocable living trust. Unlike assets that go through probate, assets held in a trust can be managed immediately by a successor trustee.

This allows your business to continue operating without interruption. A trust also keeps your business affairs private, as probate proceedings are typically public. By avoiding court involvement, you reduce delays, legal costs, and the risk of disputes.

For businesses that rely on consistent cash flow or daily operations, this strategy can make a significant difference.

Plan Ahead with Buy-Sell Agreements

If your business has partners or co-owners, a buy-sell agreement is essential. This legal document determines what happens to an owner’s share in the event of death or incapacity.

Without such an agreement, ownership could pass to heirs who may not have the skills or desire to be involved in the business. This can lead to conflict and instability.

A buy-sell agreement ensures that remaining owners can retain control while providing fair compensation to the deceased owner’s family. It creates clarity and prevents disputes at a time when emotions are already high.

Strengthen Financial Protection with Insurance

Insurance plays a key role in maintaining stability during probate. Life insurance, for example, can provide immediate funds to cover expenses, pay off debts, or support ownership transitions.

Key person insurance is another valuable option. If your business depends heavily on one individual, this type of policy helps offset the financial impact of their loss.

Having financial resources readily available ensures that your business can continue operating even while legal matters are being resolved.

Keep Business Records Organized and Accessible

One of the most overlooked aspects of probate planning is documentation. Disorganized or missing records can delay the entire process and create confusion for those stepping in to manage the business.

Make sure all critical documents are up to date and easy to access. This includes contracts, financial records, ownership agreements, and tax filings. It’s also important that your executor or successor knows where to find these documents and how to use them.

Clear documentation speeds up decision-making and reduces the likelihood of disputes or costly mistakes.

Consider Ownership Strategies That Minimize Probate

Certain ownership structures can help assets transfer more smoothly. For example, joint ownership with rights of survivorship allows a co-owner to automatically inherit your share without going through probate.

While this approach can be effective, it must be used carefully. It can introduce risks such as shared liability or loss of control. Professional guidance is essential to ensure this strategy aligns with your overall business and estate plan.

Address Taxes and Liabilities in Advance

Probate often involves settling outstanding debts and taxes, which can put pressure on your business. If there isn’t enough liquidity, assets may need to be sold to cover obligations.

Planning ahead can prevent this situation. Working with a tax advisor helps you estimate potential liabilities and prepare accordingly. Setting aside funds or using insurance to cover these costs ensures your business remains financially stable.

Communicate Your Plan to Key People

Even the most detailed plan won’t be effective if no one knows about it. Communication is a critical step in protecting your business.

Your family, partners, and key employees should understand your intentions and their roles in the event of your passing. This reduces uncertainty and helps everyone act quickly and confidently.

Regularly reviewing your plan with stakeholders ensures that everyone stays aligned and prepared.

Work with Experienced Professionals

Protecting your business during probate requires a coordinated approach. Legal, financial, and tax considerations all play a role, and mistakes can be costly.

An estate planning attorney can help structure your assets properly, while an accountant or financial advisor can guide you through tax planning and financial protection strategies. Their expertise ensures that your plan is both comprehensive and effective.

Take Action to Protect Your Business Today

Don’t wait until it’s too late to secure the future of your business. Start building your probate protection strategy now by speaking with an estate planning professional, setting up the right legal structures, and creating a clear succession plan. Taking these steps today can save your business from costly delays, legal complications, and unnecessary stress—while ensuring everything you’ve built continues to thrive for years to come.